Chitkara Business School Signs pact with ALPHABETA Inc for FinTech courses

Blog

January 14th, 2020

Comments

Comments

Do you always have to take higher risks to achieve higher returns?

It is a common conception that higher risk is rewarded with superior returns. But is this always valid? Historical data show that low-volatility (or low-risk) stocks have always outperformed the high-volatility stocks, which goes against the fundamental principle that risk is compensated by higher returns. This anomaly is called the Low-Volatility Anomaly (LVA). Several studies, especially those conducted on foreign markets observe the anomaly to be valid. In our study, we employ an LVA strategy on a universe of 100 stocks contained in Nifty 100 and try to find out whether it works in Indian markets.

We employ the LVA strategy by first computing the volatility over a six-month period for all the stocks in the universe. Here when we talk about volatility, it is nothing but the standard deviation of the daily returns for 6 months historical data. The stocks are then sorted according to their volatility. We buy the stocks in the bottom decile (stocks with low volatility) and short the stocks in the top decile constructing a market-neutral portfolio and hold for six months. The initial investment is taken to be INR 100,000 and the portfolio is rebalanced at the end of every six-month period. We start our analysis from the second quarter of the year 2011 and evaluate the performance of the strategy at the end of 16th December 2019.

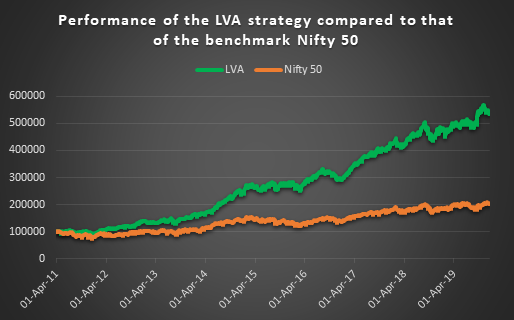

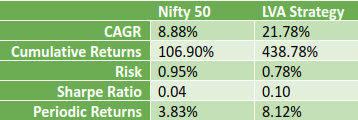

The results of our study are described in the chart above. The shorting of stocks and the market-neutral(long short together) portfolio did not perform well and therefore their performance is not shown in the chart. The performance of the strategy with the ‘long only’ scenario is compared with the benchmark. It is seen that the strategy consistently outperforms the benchmark over the analysis period undertaken in this study. The table below quantifies the performance of the LVA strategy. We see that the CAGR achieved with LVA strategy is more than twice of the CAGR of Nifty 50. Without adjusting for inflation, a Rupee invested using the LVA strategy would have reached a value of INR5.4, as compared to a value of INR2.1 that Nifty 50 reached. It is important to note that the LVA strategy outperforms the benchmark by being less risky, which is evident from the table below.

The study shows that the usual concept of risk-reward is not always valid and that it is possible to achieve superior returns while being less risky. There are various studies that try to explain why high-volatility stocks have a higher demand even when historical data shows that low-volatility stocks perform better. One explanation is that fund managers tend to focus more on outperforming in the bull markets and thus go for high-beta stocks, but in the process lose sight on the performance in bear markets. In the study, we also conclude that the inverse of the LVA is not true for Indian markets for analysis period considered, i.e., shorting high-volatility stocks did not give good returns.