Chitkara Business School Signs pact with ALPHABETA Inc for FinTech courses

Blog

April 7th, 2020

Comments

Comments

A wake-up call for a disciplined investment approach – Will COVID 19 event, bring a positive change in investors behavior?

The need for a disciplined investment approach, with ideal asset allocation and rebalancing strategy is unfortunately realized only when the market goes through a distress time like the current scenario of COVID 19 crisis. While one might argue that, the Global COVID 19 crisis is a Black Swan event, which can’t be predicted, history repeats for itself and the market goes through these cycles and events at least at once in a decade. In 2008, the liquidity crisis and now in 2020, with the COVID-19 crisis, Investors with huge allocation to equity and retiring in 2020 and 2021, are caught off handed with the fall in the market value of the portfolio. With the depletion of the market value of the equity holdings, investors are left with lower corpus to face the retirement life.

On the other hand, lower interest rate regimes, corporate defaults, cooperative banks defaults on payment of fixed deposits, haven’t furthered cause of investing and allocating the corpus towards fixed income earning instruments. The return from these asset classes, are returning towards a historical low and not meeting the inflation rates. So, what should be ideal asset allocation model and the asset class one has to invest in, so as to tide through these scenarios.

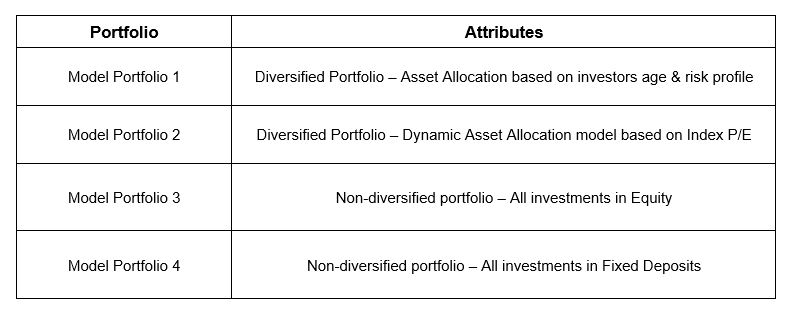

We ventured out to answer this, conducted a research, on last twenty years performance of the asset classes1 - Equity, Government Securities, Corporate Debt, and Gold. Our research has provided some interesting insights and conclusions. For the purpose of our research, we created four model portfolios. Two model portfolios with investments across asset class and proper diversification strategy and two model portfolios with no asset class diversification strategy.

Our research concludes that, dynamic asset allocation model portfolio, which involves buying when the assets are cheap and selling when the assets are costlier, coupled with re-balancing of the portfolio once in a three years’ time frame, provides better risk adjusted returns with consistent performance as compared to any other model portfolio.

For our purpose of research, we have considered

- NIFTY 50 index as for performance of Equity asset class,

- 10-year NIFTY Government Securities index for performance of Government Securities 2

- Fixed Deposits of State Bank of India, as a performance of investments in Corporate Debt,

- Gold prices as published by Indian Bullion and Jewelers Association (IBJA) sourced from Reserve Bank of India, for performance of Gold as an asset class.

Important considerations while deciding the investment strategy

Before we get into our research findings and conclusions, we have provided an overview on how investors can ideally allocate their investments across various asset class options. And what rules one can adopt to stay diversified at all times. In this, there are two important considerations- number one is to determine the asset allocation ratio and secondly, rebalancing of the portfolio.

A. Determine the asset allocation ratio:

As the saying goes, “Don’t put all your eggs in one basket”, it is very true in managing one’s investment. The first and foremost rule in investment is to maintain a proper asset class allocation and diversification strategy, while investing and determining the basket of assets one can invest in. The common investment avenues which can be availed by investors are Equity, Corporate Debt (including Fixed Deposits in Banks), Government Bonds and Commodities (like Gold).

But the question comes in, what should be the ideal model, which should be adopted in determining the asset allocation ratio. There are two asset allocation models which investors can adopt.

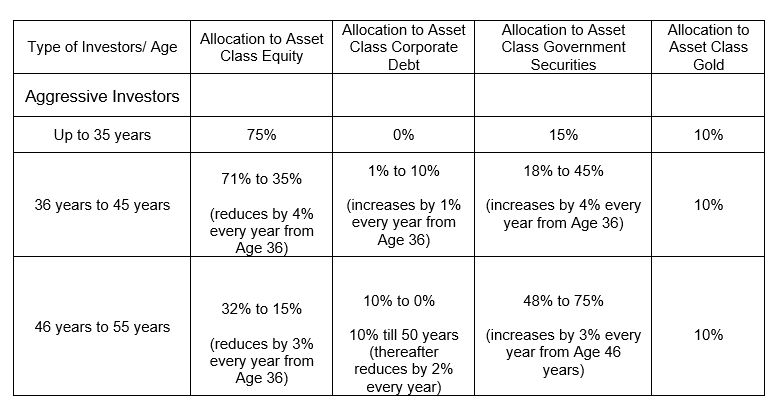

Asset Allocation Model 1: Investment allocation ratio based on investors age and risk appetite. As a rule of thumb, younger the age and higher risk appetite, higher the ability to take risk and hence, higher the allocation to asset class like Equity. The National Pension Scheme 3 provides some guidelines, for asset allocation, for an investor with high, medium and conservative risk appetite. For example, for investors with higher risk appetite, the recommended asset allocation of 75% in equity (till the age of 35 years), which gradually reduces to 15%, at the age of 55 years. Similarly, asset allocation model for a moderate and for a conservative investor.

Secondly, study has proven that, it is always advisable to keep at least 10% of the portfolio in Gold as an asset class. With increasing options of holding Gold in liquid format, like Sovereign Gold Bonds, Gold ETFs, it now easier to buy and hold Gold as an asset class with lower transaction cost and better liquidity.

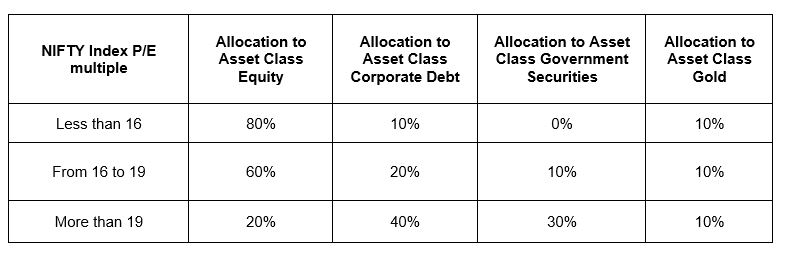

Asset Allocation Model 2: Dynamic asset allocation ratio is based on the criteria, whether the asset is cheaper to buy. Assets which are cheaper to buy, are provided higher allocation and assets which are costlier, lower allocation. As an example, for Equity asset class, one rule of thumb, investment managers use to determine, whether the equity is cheaper to buy is to review the Price/Earnings multiple of the index. In the table below and for the purpose of our analysis, we have considered the NIFTY 50 P/E multiple to determine the asset allocation model. This model is a contrarian model, like as Warren Buffet says, “investors should be fearful when others are greedy and greedy when others are fearful”.

B. Re-balancing of the portfolio

The investments based on the recommended model portfolio, can result in tilting of the recommended asset allocation ratio, a better performing asset class over non-performing asset class. The goal of the model portfolio recommendation is that, the exposure of the investments, in each of the asset class should at least on periodic interval mimic the recommended allocation ratio.

Under model 1, the rebalancing of the portfolio is done at least once a year, as the model is based on the investors age and risk appetite. In model 2, based on dynamic asset allocation, the re-balancing is performed once in three years, so as to lower the tax burden for the investors.

Scope of the research

While these are recommended asset allocation models, we ventured out to validate, the performance of the two-asset allocation model is stated above. And in addition, for the purpose of our research, we created two additional model portfolios, with no asset class diversification strategy and investments only in one asset class Equity or Corporate Debt (in our case fixed deposits).

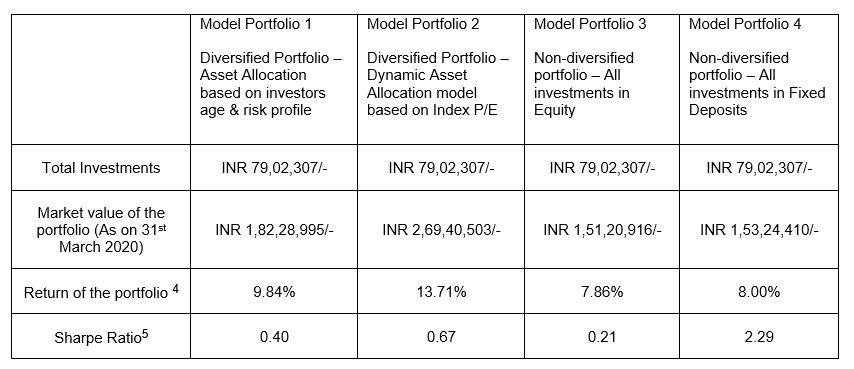

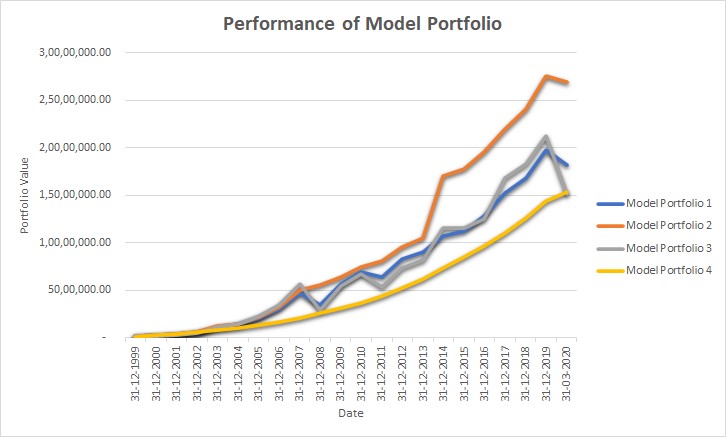

In our research, we back tested the performance of each of the model portfolio, for the last twenty years starting from the year 1st Jan 1999 till 31st March 2020.

For the purpose of our back testing, we assumed an investor at the age of 24 years on 1st Jan 1999, starts investing INR10,000/- every month, in each of the Model portfolio. The investment amount will be incremented by 10% at the beginning of every year. Say for example, the monthly investment amount will be INR 11000/- in the year 2000 and so on.

Performance of the Model portfolios

In our analysis, the performance of the Model Portfolio 2, with the dynamic asset allocation model, performed superior as compared to any other model portfolios. Followed with One can accomplish,

Conclusion:

The submission from this research is that, one needs to diversify the asset allocations for investments in order to generate a superior return which can tide through difficult times. In our research, both the diversified portfolios performed better as compared to non-diversified portfolio. While one might put forth the case that, equity always provides a higher return in the longer investment horizon, it doesn’t tantamount of allocation of 100% of the investments in Equity as an asset class. Likewise, allocating 100% of the investments in a lower risk asset classes, like fixed deposits aren’t advisable either, as the returns from these investments, most often than not, don’t even meet the inflation rates, leave alone the inflation specific to the investor goals.

Investors in order to avoid the liquidity risk and these Black Swan events like COVID-19 scenario, should always consider a proper asset allocation model while investing and periodically review and re-balance portfolio, at least once in three years.

Notes:

1 Investments in Real Estate through REITs is a viable alternative which is emerging, however with the lack of reliable historical data, we haven’t considered this asset class.

2 For the purpose of our analysis, we have considered the performance of NIFTY 10-year Benchmark G-Sec as a proxy for the performance of Government Securities

3 National Pension Scheme provides asset allocation for Moderate and Conservative customers. For the purpose of our analysis, we have considered the asset allocation for an aggressive life cycle as a proxy.

4 Computed based on XIRR Returns from the portfolio

5 Sharpe ratio is used measure the return of an investment compared to its risk.