Chitkara Business School Signs pact with ALPHABETA Inc for FinTech courses

Blog

November 5th, 2020

Comments

Comments

Is Value Investing Dead?

Value Investing is all about investing in stocks where the current market price of the stock is lesser, compared to its intrinsic value. Intrinsic value is nothing but the present value of all the expected future cashflows from the stock. Estimation of the intrinsic value involves critical analysis of a firm’s financial statements, growth prospects, industry of operation, cashflows and quality of management and make an informed decision on the expected future cashflows. One arrives at a positive investment decision, when the current market price is less than the intrinsic value. Oh yes, it involves decent amount of time to evaluate a stock, at least the time we spend equal to the research we do, before we buy a new mobile phone.

It makes logical sense to evaluate a stock or for that matter any investment opportunity, using the value investing approach since it is built on the concept of buying an asset when it is cheaper. However, with the advent of high frequency trading and subsequent growth of quantitative investment managers, the performance of Value investing style has become a debatable topic these days. Many investors are of the opinion that - “In today’s world of investing driven by algo trading, patterns and high frequency trading, Value Investing is no more relevant and is dead”. Is it really true?

We ventured out to try and answer this question for Indian market, if there are any patterns that we can observe based on the historical performance of a Value Investing portfolio. For the purpose of our analysis, we looked at performance of a Value Investing portfolio as against the performance of a portfolio based on the Growth style. As contrary to Value Investing, a Growth style portfolio invests in stocks which trade at a premium and where the current market price is higher than the intrinsic value.

To remove any selection and data snooping bias, we looked at the performance, both under the passive and active investment management styles:

- Scenario 1: Under Passive investment style, for the purpose of our analysis, we compared the performance of NIFTY Value Index, with the NIFTY Growth Index, during the time period, 1st Jan 2009 to 30th September 2020.

- Scenario 2: Under Active management style, for purpose of our analysis compared the performance of funds with Value investing objective vis-a-vis funds with Growth style.

Our results show that, in both the passive and active investment styles, the CAGR (Compounded Annual Growth Rate), for a value portfolio is higher than the CAGR of the Growth Portfolio for the period 1st Jan 2009 to 30th September 2020.

However, there are periods, which represent the economic and market cycles, where the Value portfolio underperformed the Growth portfolio. Investors who can spot these cycles, can make an appropriate investment decision, periodically re-balance the portfolio and ride on the cycle. Most often than not, no one can predict the future with 100% accuracy. Investors with long term investing strategy, are better off investing in the Value portfolio. Value Investing is all the more relevant now than historically. Lastly, fund managers or investors, who are able to generate a positive higher alpha belong to the Value investing style.

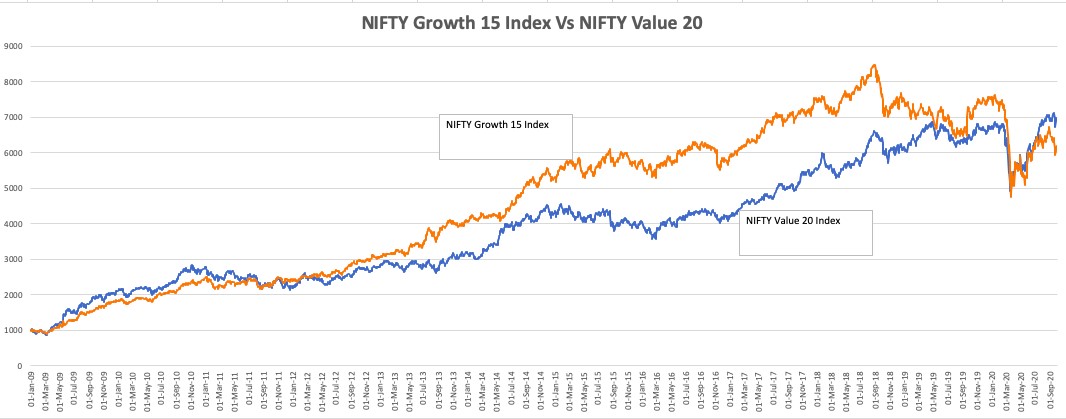

Results of Scenario 1: Passive Investment Style - Performance of Nifty Value Index v/s. Nifty Growth Index

For the purpose of our analysis, we looked at the performance of two indices, the index based on the value criteria - NIFTY 50 Value 20 Index and the index based on Growth criteria - NIFTY Growth Sectors 15. NIFTY50 Value 20 Index comprises of top 20 companies, within NIFTY50, with low P/E (Price to Earning), low P/B (Price to Book), high return on capital employed and high DY (Dividend Yield).

NIFTY Growth Sectors 15 provides investors exposure to stocks, which are of market interest. The constituents in this index, are decided based on stocks with high P/B, high P/E, consistent earnings per share growth rate and stocks with high liquidity.

Both these indices have a base date of 1st Jan 1999. The charts below shows the performance of each of the indices and the yearly performance of these two indices.

Pic: Results of Scenario 1: Passive Investment Style - Performance of Nifty Value Index v/s. Nifty Growth Index

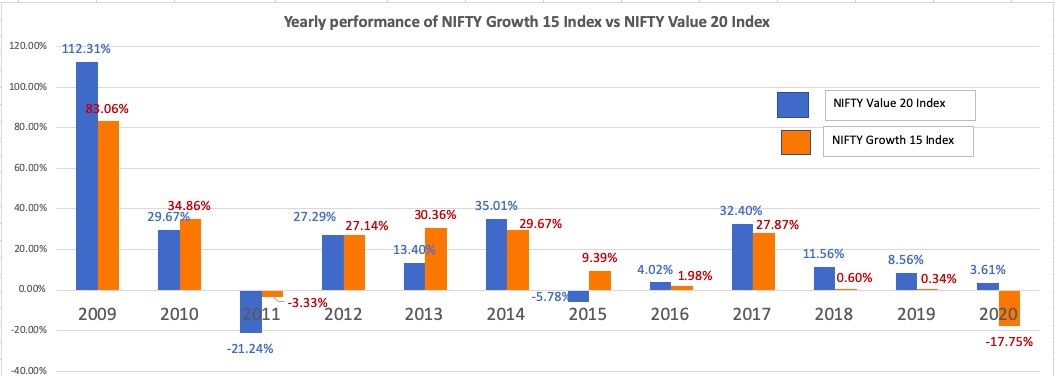

Pic: Yearly Performance of NIFTY Growth 15 TRI Index Vs NIFTY Value 20 TRI Index

If one looks at the yearly performance of Value index vs Growth index. Out of the 12 years of the observation period, starting from 1999 till date, NIFTY Value 20 has outperformed the NIFTY Growth 15 index in 8 out of those 12. In other words, if there are two investors one investing in Growth 15 Index and another investor investing in Value 20 index, the Value investor would have outperformed the growth investor, in 8 years out of 12 years. Secondly, the CAGR (Compounded Annual Growth Rate) of NIFTY Value 20 index (Total return), during the same period is 17.94% vs NIFTY Growth Index 16.77%. Under the passive investment style, Value Index has outperformed the Growth index.

There have, however, been cycles, where Growth outperforms Value. During the time period2014 to 2015, there was lot of euphoria in the market with the change of Government and lot of expectations from a bullish Economy. Reverse is true for underperformance of Growth Index during the period 2018-2020, when the Economy were going through a correction and recovery cycle.

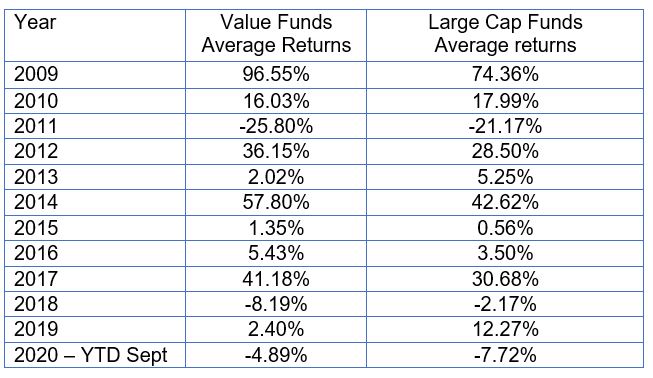

Results of Scenario 2: Performance of Value Mutual Funds Vs Large Cap Funds adopting Growth Style

In this hypothesis, we reviewed the performance of Value or Contra mutual funds, with the performance of Large Cap funds, where the active fund managers adopt the investment style as growth. Our period of comparison is similar to the one in the passive investment style, 1st Jan 2009 to 30th September 2020. Here again to avoid any data snooping bias, we looked at the performance of all the funds in the category.

The funds in the Contra/Value investing basket were selected based on two criteria. They should be in existence from 1st Jan 2009 and should adopt the investment objective of Value Investing style. In total, there were 9 funds in this category.

Similarly, the universe for Large Cap funds, was selected based on two criteria. The funds should be in existence from 1st Jan 2009 and the fund managers should have adopt growth style of investment. In total, there were 16 funds in this category.

The investment performance of these two baskets were compared against two criteria, the average and the median performance of the basket.

The table below shows the performance of both the baskets -

Table: Performance of Value Funds Vs Large cap funds with Growth investment style

The average performance of Value funds category was higher than the average returns of the Growth style large cap funds, in 7 out of 12 observation periods. The conclusion is very similar as in the passive investment strategy.

In today’s trading world, while no one can deny the exponential growth of algo trading and the dominance of the machine-based and quantitative investment strategy, Value investing still holds an edge if an investor's objective is to create long term wealth creation. Our analysis of both passive and active investment style has proven the long-term performance of the Value strategy over the growth strategy. However, if one has to adopt a Value Investing strategy, it requires a disciplined approach in the analysis of the investment avenues.

As Warren Buffett says, “We don’t have to be smarter than the rest. We have to be more disciplined than the rest”. Value investing demands nothing but a disciplined approach towards investing and it’s relevant in any day and age.