Chitkara Business School Signs pact with ALPHABETA Inc for FinTech courses

Blog

June 1st, 2020

Comments

Comments

Gilt Funds: A cushion for volatile times

The default of IL&FS and DHFL had created a bubble of uncertainity and made investors cautious towards the credit and debt market in 2018. Unfortunately, more was still to come. Recently, the Franklin Templeton fiasco brought into limelight the risks associated with India’s debt market which, above anything else, is highly illiquid. The investors at the time of investment are given the confidence that funds can be liquidated any time they wish to, but the events that happened in 2008, 2018 and now again, have failed to fulfil the promise of the said liquidity.

Current fund inflows:

Investors have been on a “risk-off” mode during the last few weeks. Equities are deemed sensitive to the vagaries of the stock market, while investment in government securities is considered to be a safety play. According to AMFI, inflows into equity schemes, including equity-linked savings schemes (ELSS), hit a four-month low of INR 6,411.88 crore in April 2020, down 47.3% from the previous month. It was expected to slow down in the current situation when both, the nation’s, and the global economy is looking at an impending recession. Growth forecast has been downgraded on account of country wide lockdown and the general uncertainty and malaise that has hit everyone on account of the ongoing pandemic is finally taking a toll on investor behaviour and choices

One asset class seems to be weathering the market volatility storm well

Gilt Funds have gained significant attention in the past few months as lower interest rates have led to robust returns. In fact, the gilt category received inflows of INR 2,515.61 crore in April 2020 compared to INR 746.71 crore a month before. At the end of April this year, the assets under management in gilt funds stood at INR 12,014 crore, 59% more than last April’s asset base of INR 7,545 crore.

What are Gilt Funds and how do they work?

Gilt funds are debt funds that invest primarily in government securities. Government securities are those instruments where the security of payment in future is borne by the national government. To bridge the deficit in revenue through taxes and the amount spent, governments raise money through bonds. These become government securities.

Recently, the Indian Government has announced a INR 20 lakh crore stimulus package which is 10% of our GDP. The government increased its borrowing by 50% from INR 7.8 lakh crore to INR 12 lakh crore to provide enough liquidity in market which has almost come to a standstill due to the virus-induced lockdown. Ideally, governments get revenue from tax but in the current economic scenario where 75% economy has been shut down for months, immediately raising taxes will not be ideal. Fiscal measures have to be kept in check keeping in view the growing fiscal deficit. The last resort is to get the monetary policy measures that help provide stability to the economy. Monetary policies are taken care of by the country's apex bank – the Reserve Bank of India in our case.

Government securities’ prices and yields are inversely related. When interest rates rise, bond prices fall. This is because when interest rates rise, investors can get a better rate of return elsewhere, so the price of original bonds adjust downward to yield at the current rate. Bond yield can be used as a parameter to assess an economy’s health. In times of a recession or when the economy is growing at a slow pace, the central bank generally reduces interest rates to increase money supply and stimulate growth. In times of market uncertainity Investors prefer security of their investments and therefore in wake of the fear of losing value in the stock market they accept low interest rates and the demand for government bonds increases.

Gilt funds portfolio holds a basket of these government securities which may have different maturity. These funds look for capital apprecialtion through the increase in prices of the underlying government securities as well as earn regular interest income from the same underlying. Portfolio managers can adjust the portfolio of these Gilt Funds by modifying the underlying Government securities that the fund holds based on the external environment.

Role of RBI in raising government securities

RBI gives loans to the government and issues ‘government securities’ for a fixed tenure to collect funds from insurance companies or banks. On maturity, the lenders give back the G-securities and are paid their money back. Debt funds were introduced to the Indian mutual funds industry in 1994. Kotak Mahindra Asset Management Company launched India’s first gilt fund in December 1998. Initially, investing in government securities was beyond the reach for retail investors, as large sums of investment were needed. Gilt funds allow retail investors to invest in such securities

- Credit Risk: The Gilt funds are backed by the government and governments usually do not default except in certain exceptional scenarios. So unlike corporate bonds, gilt funds carry significantly lesser credit risk

- Interest Rate Risk: Interest rates and prices of government securities are inversely related. Hence, in times of lower interest rates, these securities become even more attractive. Longer term securities benefit the most from lowering on interest rates

Economic growth and bond yields

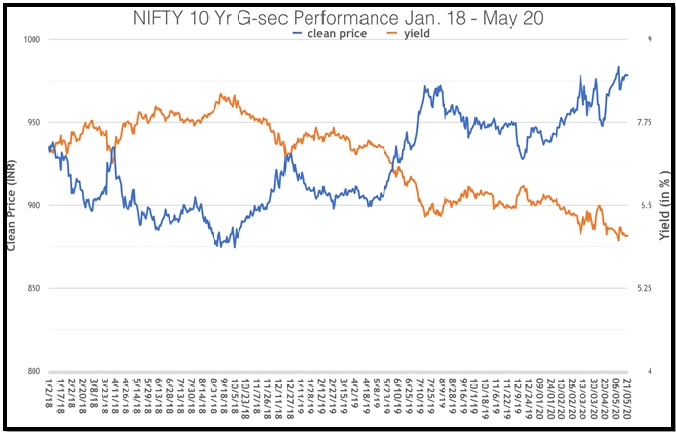

There is an observed trend between economic growth and bond yields. As we had mentioned earlier, as growth in an economy slows, interest rates generally fall, leading to an increase in bond yields. We can see this by plotting the performance of the NIFTY 10-year benchmark G-sec Index during the various phases of the Indian economy.

(Chart taken from NSEINDIA Archives, Black line indicates clean price and blue line indicates yield movement)

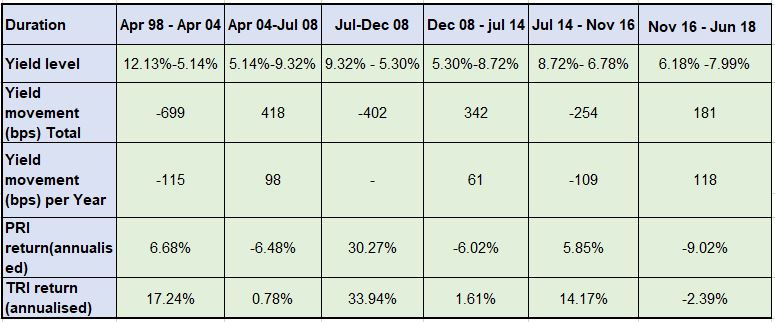

Phase 1: April 1998 to April 2004 - This phase marked a slowdown of the GDP growth from 6.2% in 1998-99 to 3.9% in 2002-03. Inflation also declined during the period. Hence, we could see the effects of the softening of interest rates with total returns ~17.24%.

Phase 2: April 2004 to July 2008 - The GDP rose from 7.8% in 2004-05 to 9.8% in 2007-08 and inflation also increased to 6.7% in 2007-08. In order to control inflation, interest rates were increased by RBI. This correlates to an increase in bond yields and considerably lower Total returns ~ 0.78%

Phase 3: July 2008 to December 2008 – This was a massively uncertain period when the global financial crisis began impacting the developing world as well. GDP growth in India reduced to 3.9%. And led to a sharp decline of interest rates of ~400 bps within 5 months. The drop in interest rates correlate with higher PRI (Price return) of close to 30.27%

Phase 4: December 2008 to July 2014 – Slowly and steadily the GDP growth increased from 3.9% in 2008-09 to 6.4% in 2013-14. The interest rates surged subsequently, which resulted in a measly rise of 1.61% in returns for the G-secs.

Phase 5: July 2014 to November 2016 – On an almost flat GDP growth, yields fell by ~250 bps and G-sec index recorded close to 14% returns during this period.

Phase 6: November 2016 to Jun 2018 – After the demonetization initiative and launch of a nationwide GST, the GDP slowly started showing signs of improvement. RBI tightened the interest rates and for the first-time negative returns were marked for the G-secs

Phase 7: June 2018 – May 2020- Nifty 10 Yr Gsec index gave a PRI (price return) of close to 10% during this phase. RBI has shaved off 2.25 percentage points from the repo rate between Feb 2019-May 2020 in its efforts to induce liquidity in the market to revive the economy. According to various research reports, India’s economic growth forecast for FY 2020-21 is being estmated being the lowest since the economy was opened up ~30 years back. The inflation numbers are uncertain on account of demand and supply chain disruptions caused by lockdown.

The current scenario

The Government of India and the RBI have taken a calibrated approach in announcing a large stimulus that the country needs right now to be back on the growth track. With a fear of Indian economy going into recession, there is a high possibility of more monetary measures in the form of interest rate cuts by the RBI to bolster growth. This can benefit the Gilt funds as prices of underlying securities are bound to increase with these rate cuts. Also keeping in mind the low credit risk associated with these funds, Gilt funds present a good investment opportunity.