Chitkara Business School Signs pact with ALPHABETA Inc for FinTech courses

Blog

December 23rd, 2019

Comments

Comments

All hail the new 'Bond' - The Bharat Bond ETF

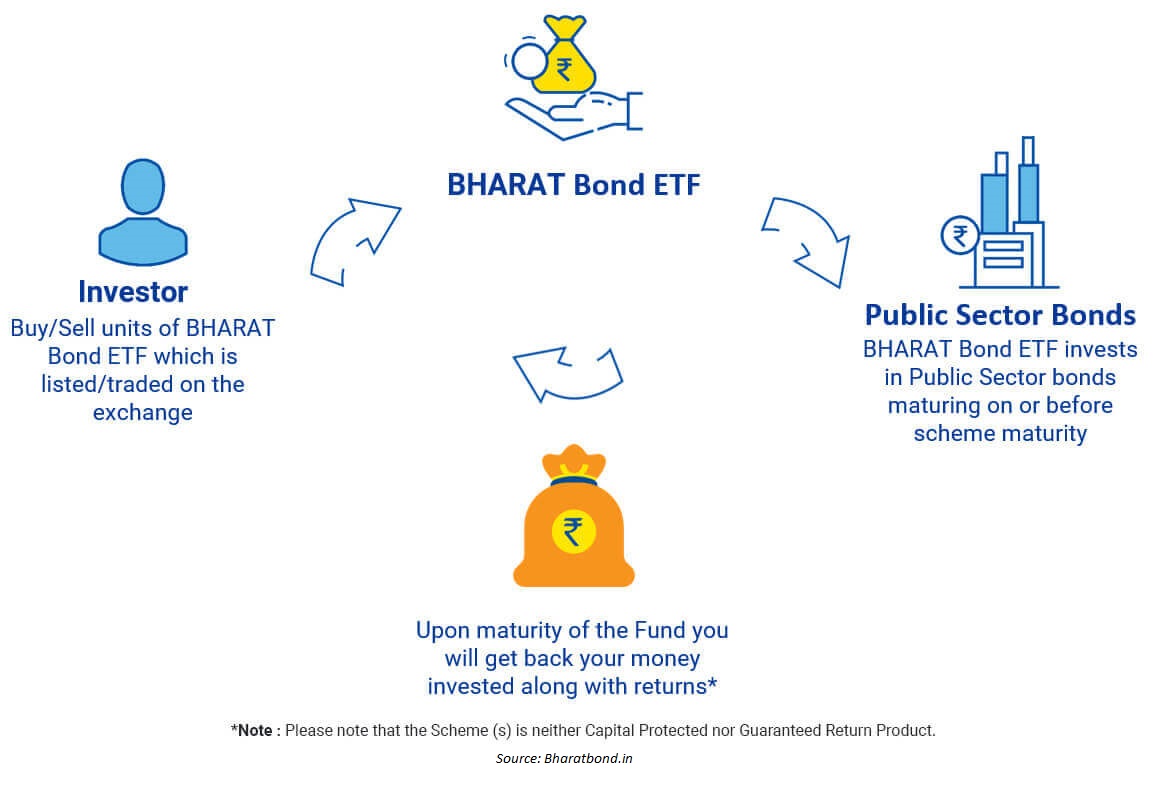

All fixed income investment lovers have a new reason to rejoice. They are celebrating the introduction of the Bharat Bond ETF - the first corporate bond ETF which marks the emergence of a new class of investment in India. Bharat Bond ETF is a debt exchange traded fund (ETF) that will hold only bonds issued by public sector companies owned by the Government of India. It is an initiative by the Government of India to help public sector organisations with their borrowing requirements and at the same time give an opportunity to retail investors to access the bond market in an easy and liquid manner. Earlier, bond issuances were done through private placements and a minimum amount of Rs. 10 lakh was required to be invested. This excluded small retail investors from participating in the bond market due to liquidity and accessibility constraints. The Bharat Bond ETF allows small investors to invest a minimum of INR 1,000, hence creating a potential opportunity for all investors to get more returns from the Bond ETF as compared to a bank fixed deposit.

What is the Bharat Bond ETF?

Structure of the Bharat Bond ETF

The Bharat Bond ETF will invest in a basket of bonds with AAA credit rating issued by Central Public Sector Undertakings (CPSUs) Central Public Sector Enterprises (CPSEs), Central Public Financial Institutions (CPFIs) any other Government organisation bonds. An interesting feature about this ETF is a designated fixed maturity date. Bharat Bond ETF comes in two variants - 2023 maturity ETF and 2030 maturity ETF. Upon maturity, the investor will receive the principal plus interest earned at the time of maturity. So, does that mean there is a lock in period for 3 years and 10 years? No, investors can sell the units like a stock on the stock exchange during market hours (just like how a stock ETF trades).

The Bharat Bond ETF is a passive fund which will track the NIFTY Bharat Bond Index. The index is created and maintained by NSE and will be free from any active fund manager bias (for now will be managed by Edelweiss Asset Management). The asset management company will keep launching new series every year - for example, ETF 2024 will be launched in 2021 with a three year maturity, similarly Bharat Bond ETF 2031 will be launched in 2021 with a 10 year maturity. Every year a new ladder of Bond ETF will be created which will start maturing every year starting from 2023.

Will there be re-balancing?

The entire series will not constitute the same basket of bonds throughout. The index will be rebalanced on a quarterly basis by NSE and downgraded constituents will be taken out of the index during re-balancing. The constituent will be excluded from the index if the rating falls to lower than “AAA” or if it ceases to be a CPSE.

How does a Bond ETF behave?

Before going ahead, let’s talk about ETFs. An exchange traded fund is a mutual fund that trades on exchange just like a stock. It is a passive investing instrument, for example, the NIFTY50 ETF replicates the index. ETFs normally are open ended and do not have a maturity date. They trade as long as their listing continues on the exchange. But the Bharat Bond ETF comes with a fixed maturity date which provides accountability and transparency.

So, is it like a mutual fund then? Not really...

When we invest in mutual funds, the asset management company for the fund collects the orders from investors till 2pm and then buys the stock(s) and discloses the current day NAV (Net Asset Value) after 9pm. In contrast, an ETF NAV or price can be seen live during the day. As mutual funds are actively managed by the fund managers, they charge an approximate 2% as fund management fee, whereas ETFs come at a low cost of about 0.5%. In case of Bharat Bond ETF it cost even lower (0.0005%)!

To get to know more about mutual funds and ETFs, please refer to our earlier article on the same.

A win - win solution for both investors and state-owned companies?

For state-owned companies, the Bharat Bond ETF will expand the investor base and will increase the demand for their bonds which will allow the issuer(s) to borrow at a reduced cost and help reduce borrowing cost over a period of time. This will add a new source of funding for these companies. For investors, it is expected to provide a predictable tax efficient return and low cost access to the Indian bond market.

Are their any associated risks?

Default risk - when company doesn’t pay back its debt. Since Bharat Bond ETF portfolio will constitute of bonds issued by PSUs, there is very minimal default risk as PSUs have an implicit sovereign guarantee. Remember the example when the Government had to come and recapitalize the national banks.

Interest rate risk, however, remains. As interest rates rise or fall, the yield of the underlying bonds will rise and fall. Only, if the ETF is being held till maturity, the risk will be negated. Also Interest rates in India are close to a multi-year bottom, so locking at these levels may not be very rewarding especially for the long term 10year+ variant.. If PSU borrowing rates go up in future, investors in this ETF would missout an opportunity to earn better rates.

Liquidity Risk - As mentioned earlier, the Bharat Bond Index will be rebalanced every quarter. If a constituent is dropped from the index, the ETF will be obliged to sell off the holdings (bonds) issued by that constituent. This may pose a major risk since the Indian debt market is not that liquid. Also in the secondary market, debt ETFs historically have not had high liquidity. So selling the units of this ETF in the secondary market may also be a little difficult. Bharatbond website claims that they have appointed a market maker to provide liquidity on the exchanges and investors can buy/sell their ETF units on the exchange at any time they wish

Conclusion

Bharat Bond ETF is an initiative to promote the retail participation in the Bond market and enable Government borrowings for infrastructure and nation building efforts.This ETF is a good investment option for investors looking for asset class diversification, better yields than fixed deposits and longer holding period till maturity. But,there are pertinent issues, the secondary market for Bond ETF in India is not liquid, and this issue remains to be seen, whether it will be any different. Low liquidity would also mean associated transaction costs will be higher. Secondly, the interest rates in India are at a multi-year low. Locking the investments at these levels for a higher term to maturity, might not be a wiser investment option.